- Maximizing Your Investments: Top Assets for Small Budgets - June 20, 2023

- Investing Made Easy: A Beginner’s Guide to Index Funds - March 30, 2023

- Do Index Funds Have Fees? [Don’t Overpay] - March 21, 2023

In my previous 3-fund portfolio post, I went into depth about what the 3-fund portfolio is and how it can benefit you. If you haven’t already read it, go ahead and read that post first, then come back to this one.

In this post, I’ll show you exactly how you can build a 3-fund portfolio with Fidelity.

We’ll briefly review what a 3-fund portfolio is, and why it’s beneficial, then dive into which Fidelity Index Funds you should use to build your portfolio.

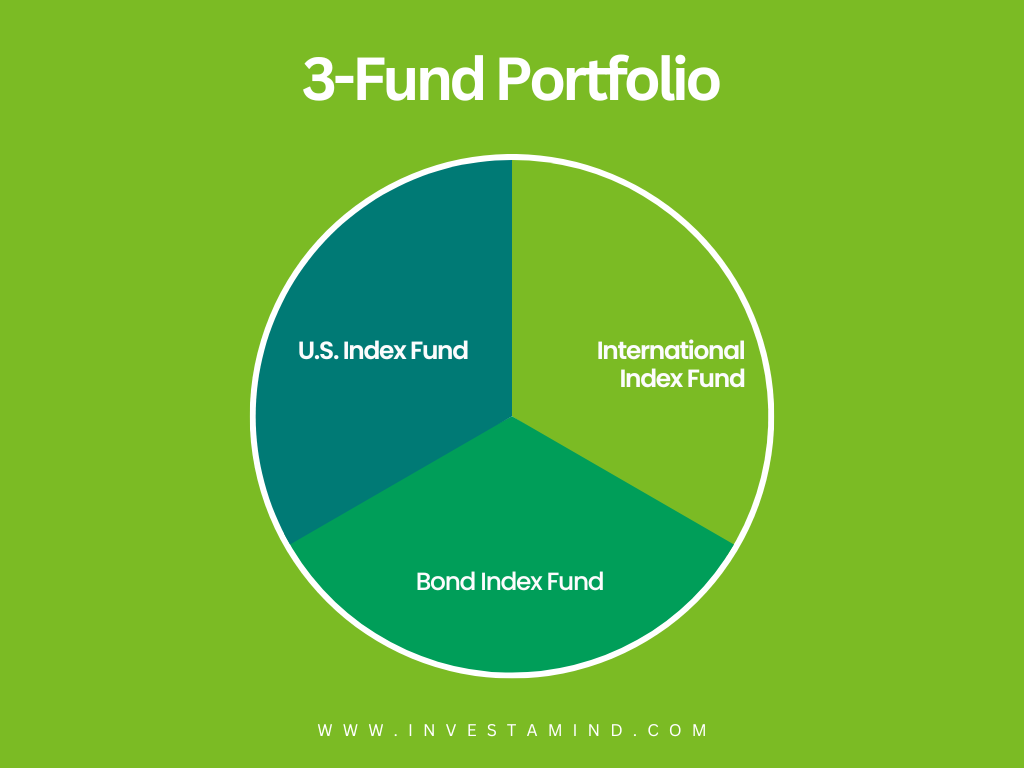

What is a 3-Fund Portfolio?

Created by the Boglehead’s community, the 3-fund portfolio is probably one of the best passive investing strategies for the stock market.

Just like the name implies, this strategy only consists of investing in three simple index funds:

- A domestic stock market index fund

- An international stock market index fund

- A domestic total bond fund

Why is the 3-fund portfolio strategy beneficial?

There are several reasons why you should consider using the 3-fund portfolio as a part of your investment strategy. Let’s go over a few reasons.

It provides global diversification

Because a 3-fund portfolio consists of a domestic index fund, and an international index fund, you are essentially investing in the global stock market.

A typical “total domestic index fund” contains around 4,000 stocks and attempts to replicate the returns of the entire U.S. stock market.

When you invest in a total domestic index fund, you’re investing in a large range of businesses – from gigantic businesses such as Apple and Google to the smallest businesses you’ve probably never heard of.

An “international index fund” provides you with diversification outside of the U.S. border. Generally containing around 5,000 to 8,000 stocks, international index funds are greatly diversified from the developed nations in Europe to developing countries such as Brazil and South Africa.

Not sure you should invest in international markets? Read my article on why you should invest internationally.

It’s cheap

The average actively managed mutual fund would cost you around 0.5% per year. That means, if you were to invest $10,000, you would be charged $50 per year.

On the other hand, index funds are passively managed, and therefore, are much cheaper to invest in. The average index fund only costs around 0.03%, which means you would only pay $3 to invest the same $10,000.

You may be thinking that $50 and $3 don’t seem like a big difference, but the difference adds up over the years.

Let’s say you invested $10,000 and kept that money in the fund for 30 years. Assuming a rate of return of 9%, a 0.5% fee would’ve cost you over $17,000 in fees, whereas a 0.03% fee would’ve only cost you around $1,000.

That’s more than 17 times! Avoid actively-managed mutual funds and stick with cheap index funds.

It’s easy to manage

Managing a portfolio with individual stocks can be a headache. Not only would you have to keep up all fundamental analyses of the stocks, but you’d also have to properly rebalance the portfolio.

With the 3-fund portfolio, all you have to worry about is managing three index funds. Once you determined how much of your portfolio you want to allocate to each, you only have to worry about rebalancing it around once a year.

No need to worry about managing individual stocks – the fund managers of the index funds will take care of the rest.

How to build a 3-fund portfolio with Fidelity

Now that we covered the basics of the 3-fund portfolio and its benefits, I’m going to show you step-by-step how to build your portfolio with Fidelity Investments.

The domestic index fund

First up, you’re going to need a domestic index fund that invests in domestic stocks. There are two Fidelity domestic index funds: FXAIX and FSKAX.

FXAIX – This is Fidelity’s S&P 500 index fund. It’s a fund that invests in the top 500 companies in the United States.

FSKAX – This is Fidelity’s Total Market Index Fund. A total market index fund invests around 20% of its portfolio in mid-cap and small-cap businesses, which are smaller companies.

The difference between the two is that FSKAX invests in the entire U.S. stock market whereas FXAIX only invests in the top 500 U.S. companies.

I recommend investing in a total market index fund because it covers the whole market. However, the choice is up to you, as both index funds have yielded similar returns historically.

Domestic Index Fund: FSKAX

The international index fund

Next up is the international index fund. Fidelity has three very similar international index funds: FTIHX, FSGGX, and FSPSX.

Upon first glance, all three appear to be the same. But I’ve done some digging and found out that they’re very different.

I’ve written a whole post on my findings here, but long story short, FTIHX is the best Fidelity International Index Fund because it’s the most diversified.

FSGGX – Only invests in large-cap and mid-cap stocks. it does not invest in small-cap stocks, aka small businesses.

FSPSX – Only invests in large-cap. Does not invest in mid-cap or small-cap.

FTIHX – The only one of the three that invests in large-cap, mid-cap, and small-cap businesses.

Although all three international index funds are equally diversified in countries across the globe, FTIHX is the only fund that invests in mid-cap and small-cap.

International Index Fund: FTIHX

The U.S. bond fund

The last fund you will need for your 3-fund portfolio is a bond index fund. Fidelity has several bond index funds but the only all-round, well-diversified fund would be FXNAX.

Bonds yield a low but steady stream of consistent income every month. Think of bonds as a tool you can use to dampen volatility in your portfolio.

Bonds are in no way near as volatile as the stock market. Allocating some of your portfolio’s funds to bonds will expose less of your money to the stock market, and therefore, dampen the volatility of your portfolio.

How much you allocate to bonds is a personal decision. Everyone is different with different financial needs, but there are two main reasons why you might want to allocate funds to a bond index fund.

- You’re close to, or in retirement, and you’re living off of the funds from your portfolio. You cannot risk too much or else you’ll risk your monthly income.

- You’re risk-averse and cannot tolerate risk well without panicking.

The more you allocate to bonds, the less volatility your portfolio will experience, but the less returns you’ll get. This is because of the risk vs. reward ratio.

No matter what type of investment, risk vs. reward always go hand in hand. If you want to achieve a higher return, you have to take on more risk. And if you want to be less risky, you’ll have to settle for lower returns.

A general rule of thumb is that if you’re far from retirement, and you’re in your 20s to 30s, you usually don’t need bonds in your portfolio. When you’re that far out from retiring, you should be taking on more risk to aggressively grow your portfolio.

As you near retirement and approach your 40s, and 50s, you can start adding around 20-30% of your portfolio to a bond index fund.

Overall, use FXNAX as a tool to dampen volatility in your portfolio, but be aware that the more you allocate to it, the less returns your portfolio will experience.

Bond Index Fund: FXNAX

Conclusion

Today, we learned how to build a 3-fund portfolio with Fidelity’s index funds. The best index fund to invest within each category is the following:

- Domestic Index Fund: FSKAX

- International Index Fund: FTIHX

- U.S. Bond Index Fund: FXNAX

I hope you enjoyed today’s post. What made you go with Fidelity? How much of your portfolio are you allocating to bonds?